Health insurance premiums in the United States vary significantly — and one of the biggest factors is age.

If you’ve ever compared plans, you’ve likely noticed that premiums increase as you get older. But how much do they increase? And why?

In this complete guide, we break down health insurance premiums by age, including:

- Average costs by age group

- Why age affects premiums

- Realistic price ranges

- Ways to reduce costs at any age

Let’s dive in.

Why Do Health Insurance Premiums Increase With Age?

Health insurance companies calculate risk when setting prices. Older individuals are statistically more likely to:

- Need medical care

- Develop chronic conditions

- Require prescriptions

- Visit specialists more often

Because of this, insurers charge higher premiums to balance risk.

ACA Rule (Important)

Under the Affordable Care Act (ACA):

- Insurers can charge older adults up to 3 times more than younger adults

- This is called the 3:1 age rating ratio

👉 Example:

- 21-year-old: $300/month

- 64-year-old: up to $900/month

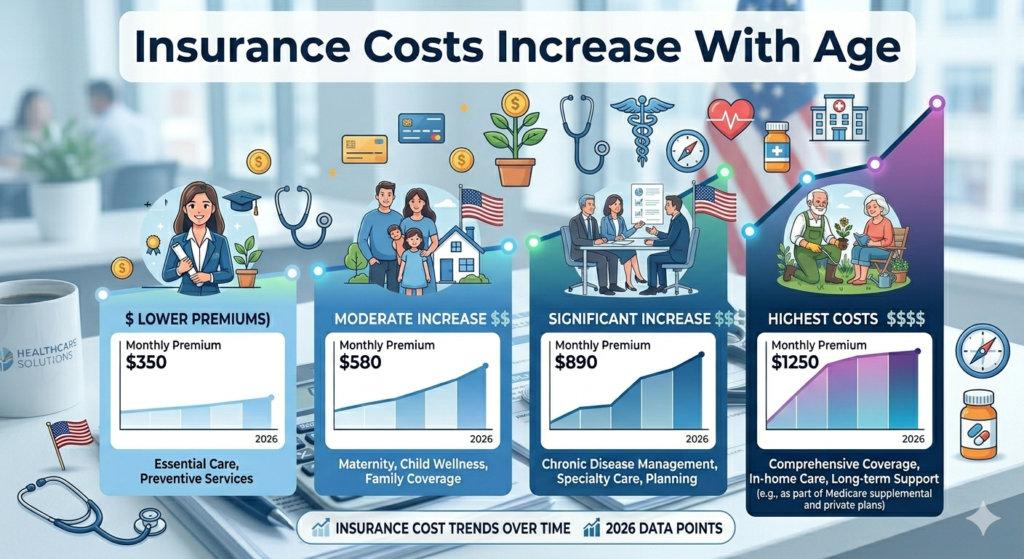

Average Health Insurance Premiums by Age (2026)

Below is a realistic breakdown based on current marketplace trends.

Ages 18–25

- Average Premium: $250 – $350/month

- Lowest cost group

- Often qualify for catastrophic plans

👉 Best for:

- Students

- Young professionals

Ages. 26–30

- Average Premium: $300 – $400/month

- Slight increase after age 26 (loss of parental plan eligibility)

Ages. 31–40

- Average Premium: $400 – $550/month

- Costs rise steadily

Ages. 41–50

- Average Premium: $550 – $750/month

- Higher risk leads to higher premiums

Ages 51–60

- Average Premium: $700 – $1,000/month

- Significant increase

Ages 61–64

- Average Premium: $900 – $1,200/month

- Highest pre-Medicare costs

Premium Comparison Table by Age

| Age Group | Monthly Premium | Annual Cost |

|---|---|---|

| 18–25 | $250–$350 | $3,000–$4,200 |

| 26–30 | $300–$400 | $3,600–$4,800 |

| 31–40 | $400–$550 | $4,800–$6,600 |

| 41–50 | $550–$750 | $6,600–$9,000 |

| 51–60 | $700–$1,000 | $8,400–$12,000 |

| 61–64 | $900–$1,200 | $10,800–$14,400 |

👉 These are averages. Actual premiums depend on location and plan type.

How Premiums Change After Age 65

At age 65, most Americans transition to Medicare.

Medicare Costs (Approx):

- Part A: Usually free (if eligible)

- Part B: ~$170/month

- Part D (drugs): $20–$50/month

👉 This often results in lower premiums compared to private insurance.

Key Factors That Influence Premiums (Beyond Age)

Age is important — but not the only factor.

1. Location

Healthcare costs vary by state.

- Higher: California, New York

- Lower: Texas, Florida

2. Plan Type

- Bronze: Lowest premium

- Silver: Moderate

- Gold: Higher premium

- Platinum: Highest premium

3. Tobacco Use

Smokers can pay up to 50% more.

4. Income (Subsidies)

Lower-income individuals qualify for tax credits.

👉 Example:

- Full price: $600/month

- After subsidy: $100/month

5. Family Size

Adding dependents increases total cost.

Health Insurance Premiums by Plan Tier (Age-Based Insight)

Bronze Plans

- Cheapest monthly cost

- High deductibles

- Ideal for young and healthy

Silver Plans

- Most popular

- Balanced coverage

- Eligible for extra savings

Gold Plans

- Higher premium

- Lower out-of-pocket

Platinum Plans

- Highest premium

- Best coverage

Real-Life Example

Let’s compare two individuals:

Person A (Age 25)

- Premium: $300/month

- Annual: $3,600

Person B (Age 60)

- Premium: $950/month

- Annual: $11,400

👉 Difference: $7,800/year

This shows how strongly age impacts costs.

Why the 3:1 Rule Matters

Before ACA reforms, older adults could be charged 5x more.

Now:

- Maximum ratio = 3:1

- Provides protection for older individuals

How to Lower Health Insurance Premiums at Any Age

Here are practical ways to save:

1. Use ACA Subsidies

Available based on income.

2. Choose High-Deductible Plans

Lower monthly cost, higher out-of-pocket.

3. Stay Healthy

- Exercise

- Eat well

- Avoid smoking

4. Compare Plans Annually

Premiums change every year.

5. Use Preventive Care

Many services are free under ACA.

6. Consider HSA Plans

Tax advantages + savings.

Best Health Insurance Strategy by Age

20s

- Choose low-cost plans

- Focus on emergencies

30s

- Balance cost and coverage

40s

- Add preventive care coverage

50s–60s

- Prioritize lower deductibles

- Prepare for Medicare

Common Mistakes to Avoid

- Choosing cheapest plan without checking deductible

- Ignoring network coverage

- Not checking subsidy eligibility

- Skipping annual plan comparison

Future Trends in Age-Based Premiums

Looking ahead:

- Premium increases may stabilize

- Telehealth may reduce costs

- Preventive care may lower long-term expenses

Final Thoughts

Understanding health insurance premiums by age helps you plan smarter.

Key takeaways:

- Premiums increase steadily with age

- ACA limits pricing differences

- Subsidies can reduce costs significantly

- Smart plan selection saves money

No matter your age, the goal is the same:

👉 Get the best coverage at the lowest total cost.

3. FAQs

1. Do health insurance premiums increase every year with age?

Yes. Premiums generally increase as you age due to higher health risks.

2. What is the 3:1 age rating rule?

It limits insurers from charging older adults more than three times what younger adults pay.

3. At what age are premiums highest?

Premiums are highest between ages 60–64 before Medicare eligibility.

4. Do premiums decrease after age 65?

Yes. Medicare often reduces overall premium costs.

5. Can I reduce premiums as I get older?

Yes. Use subsidies, compare plans, and choose cost-effective coverage.

6. Are young people required to buy insurance?

Not federally, but some states have mandates.

Disclaimer

Disclaimer: The information provided in this article titled ‘Health Insurance Premiums by age’ is for educational and informational purposes only. While we strive for accuracy and reliability, we recommend verifying details from official sources or professionals before making decisions.

Also read about,