Healthcare costs in the United States remain among the highest globally, making family health insurance pricing a major financial concern for millions of households. Whether you have coverage through an employer, purchase a plan on the Affordable Care Act (ACA) Marketplace, or buy private coverage outside the exchange, costs vary widely based on age, location, income and coverage level.

Understanding how much a family of three — typically two adults and one child — might pay for health insurance in 2026 requires an overview of all major coverage pathways, what influences pricing, tax credits and subsidies, real‑world examples, and actionable strategies to lower your expenses. This in‑depth article provides all that and more.

Introduction – Why Family Health Insurance Costs Matter

Healthcare insurance is essential financial protection against exorbitant medical bills in the U.S. But unlike many other developed countries, the U.S. relies heavily on private and employer coverage, and costs have been rising steadily.

According to the Kaiser Family Foundation (KFF), the average annual premium for family health insurance through an employer plan reached nearly $27,000 in 2025, a figure which continues to rise into 2026 as medical prices and insurance costs climb.

This high cost impacts family budgets and decision‑making, influencing everything from employment choices to whether a child’s preventive care is sought. Given how complex pricing can be, it’s critical to break down the data in a structured, practical way.

Section 1 – Typical Family Health Insurance Costs in the U.S. (2026)

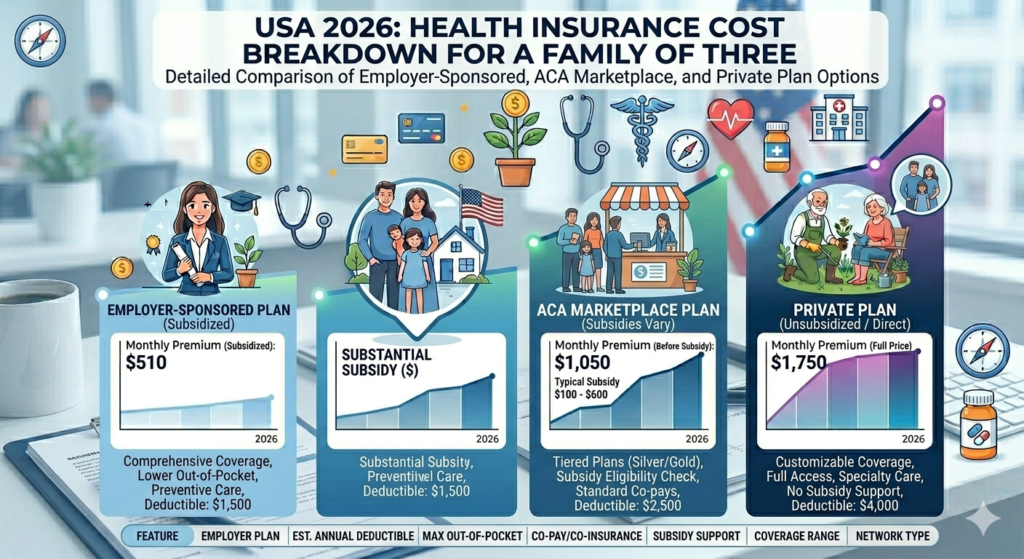

1. Employer‑Sponsored Health Insurance

Most Americans — especially working adults — receive health coverage through their employers.

Key cost figures:

- The average annual premium for family coverage through an employer was approximately $25,500–$27,000 in 2025, with most insurers expecting similar or slightly higher figures in 2026.

- Employers typically pay most of the premium: about 65–75% on average for family plans, leaving employees responsible for roughly 25–35% of the cost.

Monthly Employee Share Estimate (2026):

| Coverage Type | Average Monthly Worker Contribution | Estimated Annual Cost |

|---|---|---|

| Employer‑sponsored family plan | ~$500 – $700 | ~$6,000 – $8,400 |

These are rough estimates and vary depending on the employer’s cost‑sharing arrangement. Bigger employers usually pay more of the premium, while small businesses may pass more costs to employees.

Pros and Cons of Employer Plans:

Pros:

✔ Lower employee cost than private plans

✔ Often includes dental, vision, and wellness coverage

✔ Usually comprehensive with better networks

Cons:

✖ Plan options are limited

✖ Coverage may end if employment changes

✖ Cost share still significant, especially for families

2. Affordable Care Act (ACA) Marketplace Coverage

The Marketplace (Healthcare.gov and state exchanges) offers plans in metal tiers — Bronze, Silver, Gold, and Platinum — with costs varying significantly based on income and eligibility for subsidies.

Typical Monthly Premiums (2026, pre‑subsidy):

| Metal Tier | Family of 3 (estimated monthly) |

|---|---|

| Bronze | ~$850 – $1,050 |

| Silver | ~$1,050 – $1,300 |

| Gold | ~$1,350 – $1,700 |

| Platinum | ~$1,700 – $2,100 |

These figures are averages and vary by state, age, and insurer.

With Subsidies:

Families with income between 100% and 400% of the Federal Poverty Level (FPL) may qualify for premium tax credits that significantly reduce monthly payments, sometimes to levels as low as $0–$300 per month for lower incomes.

Example Subsidy Impact (Silver Plan):

- Family income around 150% FPL → ~$0–$50/month

- Income ~200% FPL → $150–$250/month

- Income ~300% FPL → $400–$550/month

- Income ~400% FPL → ~$700–$900/month

These subsidies are a crucial part of affordability for many middle‑income families.

Pros and Cons of Marketplace Plans:

Pros:

✔ Access to premium tax credits

✔ Standardized benefits by metal tier

✔ Available regardless of employer coverage

Cons:

✖ Premiums can be high without subsidies

✖ Deductibles and out‑of‑pocket costs vary widely

✖ Networks may be narrow

3. Private (Off‑Marketplace) Health Insurance

Purchasing a plan directly from an insurer or broker outside the ACA exchange is another option, but it doesn’t qualify for tax credits.

Estimated Monthly Costs (2026):

- Family health insurance via private purchase often falls between $720 – $1,400 per month depending on age, state, and plan design.

Private plans might offer broader networks or different benefit structures, but they tend to be less cost‑advantaged than marketplace plans with subsidies, and more expensive than employer plans for families without employer support.

Pros and Cons of Private Plans:

Pros:

✔ Flexible choices outside Marketplace rules

✔ Potentially lower cost for high‑income families

Cons:

✖ No premium tax credits

✖ Often higher premiums than employer coverage

✖ Deductibles & cost‑sharing can be high

Section 2 – Key Cost Drivers for Family Plans

Why do health insurance costs vary so much for families? Several major factors influence pricing:

1. Age and Health of Covered Individuals

Older adults and children with chronic conditions typically push premiums higher. ACA rules allow age rating, meaning older adults may be charged up to three times more than younger adults for the same plan.

2. Geographic Location

Health insurance costs vary significantly by state and region, reflecting local healthcare pricing, competition and provider networks.

3. Plan Tier (Bronze, Silver, etc.)

Higher tiers (Gold, Platinum) cost more but offer lower deductibles and out‑ofpocket expenses.

4. Subsidy Eligibility

For families qualifying for ACA subsidies, actual out‑of‑pocket premium costs can be substantially lower, reducing overall household expenses.

5. Employer Contributions

The level of employer subsidy dramatically affects the family’s share of premium costs.

Section 3 – Total Cost of Ownership: Beyond Monthly Premiums

Your true costs include not just premiums, but also:

- Deductibles: Money you pay before insurance contributes.

- Copays and Coinsurance: Charges for visits and services.

- Out‑of‑Pocket Maximums: Total cap on what you pay in a year.

For example, some ACA plans have out‑of‑pocket maximums near $18,900 for families in 2026, meaning that’s the most you could pay in a worst‑case scenario if you meet the max.

Section 4 – Real‑World Family of 3 Cost Scenarios

Here are data‑backed examples for a typical family of three in 2026:

Scenario A – Employer Plan

- Total annual family premium: ~$27,000

- Employee pays: ~$6,000 – $8,400

- Employer pays: remainder

This results in manageable month‑to‑month costs for employed families.

Scenario B – Marketplace Silver Plan (Before Subsidy)

- Monthly: ~$1,100 – $1,300

- Annual: ~$13,200 – $15,600

With subsidies, costs could drop below ~$4,000/year depending on income.

Scenario C – Private Off‑Marketplace Plan

- Monthly: ~$720 – $1,400

- Annual: ~$8,640 – $16,800

Higher for premium networks or richer benefit designs.

Section 5 – How to Reduce Family Health Insurance Costs

Families can take several proactive steps:

1. Use Employer Coverage if Available

Employer plans often offer the best net cost when subsidies aren’t available.

2. Maximize ACA Subsidies

Carefully estimate income to qualify for premium tax credits and cost‑sharing reductions.

3. Compare Multiple Marketplace Plans Annually

Premiums and subsidies change yearly — shopping can yield lower costs.

4. Choose Higher Deductible Plans if Healthy

High‑deductible plans often have lower monthly premiums and can be paired with Health Savings Accounts (HSAs).

5. Consider In‑Network Only Providers

Using in‑network doctors and hospitals reduces out‑of‑pocket costs.

Section 6 – Pros & Cons of Different Coverage Types

| Coverage Type | Pros | Cons |

|---|---|---|

| Employer‑Sponsored | Lower employee cost, broad coverage | Limited choice of plans |

| Marketplace (ACA) | Subsidies lower costs, standardized benefits | Can still be expensive without subsidies |

| Private Plans | Flexible options | No tax credits, pricey deductibles |

3. FAQs (Featured Snippet Optimized)

1. How much does family health insurance cost for a family of 3 in the USA in 2026?

For a family of three, employer‑sponsored health coverage averages about $25,500–$27,000 annually, with the employee paying roughly $6,000–$8,400 depending on employer contributions. Marketplace plans before subsidies often range from $850–$1,300 monthly.

2. Are Marketplace (ACA) health insurance plans cheaper than employer coverage?

Marketplace plans may be cheaper if you qualify for premium tax credits and cost‑sharing reductions. Without subsidies, employer coverage may be more affordable.

3. What is the average monthly premium for a family in the U.S.?

A typical family of three might pay between $850 and $1,300 per month before subsidies on the Marketplace, and significantly more without employer support.

4. Do health insurance premiums change every year?

Yes — premiums commonly increase yearly due to healthcare cost inflation and changes in medical service utilization.

5. Can subsidies make health insurance free for families?

If your income is within ACA eligibility limits, premium tax credits can significantly reduce or eliminate the monthly cost, though cost‑sharing may still apply.

Disclaimer: The information provided in this article titled ‘family health insurance cost USA’ is for educational and informational purposes only. While we strive for accuracy and reliability, we recommend verifying details from official sources or professionals before making decisions.

Also read about,