Accessing quality healthcare is a priority — but knowing how much you’ll pay for individual health insurance in the UK can feel confusing. The UK’s National Health Service (NHS) provides universal care, but many residents look to private medical insurance (PMI) for quicker treatment, specialist access, and added flexibility.

This guide unpacks everything you need to know about individual health insurance costs in the UK — from average premiums and price drivers to actionable ways to save money and FAQs designed for Featured Snippets.

Introduction: Why Cost Matters More Than Ever

In recent years, the cost of private health insurance in the UK has been shaped by rising healthcare demand, NHS waiting lists, medical inflation, and personalised pricing models used by insurers. Although not everyone in the UK opts for PMI, nearly 1 in 8 residents has private medical insurance, with thousands choosing individual policies to secure faster diagnostic services and treatments.

Health insurance cost isn’t just a number — it reflects your health profile, the quality of cover you need, your location and risk factors. This guide cuts through confusion and gives you a practical roadmap to understand, compare, and optimise your individual health insurance cost.

Section 1 – What Is Individual Health Insurance in the UK?

Private Medical Insurance (PMI) is a private contract between you and an insurer. Unlike life‑long NHS care, PMI provides faster access to treatments as a private patient — including consultations, diagnostics and hospital procedures.

Key features include:

- Specialist referrals without NHS waiting lists

- Choice of hospital and consultant

- Access to private diagnostics (MRI, CT scans)

- Elective surgical treatments

However, PMI is not a replacement for NHS care — and it doesn’t typically cover routine GP visits, dental check‑ups, or chronic disease management.

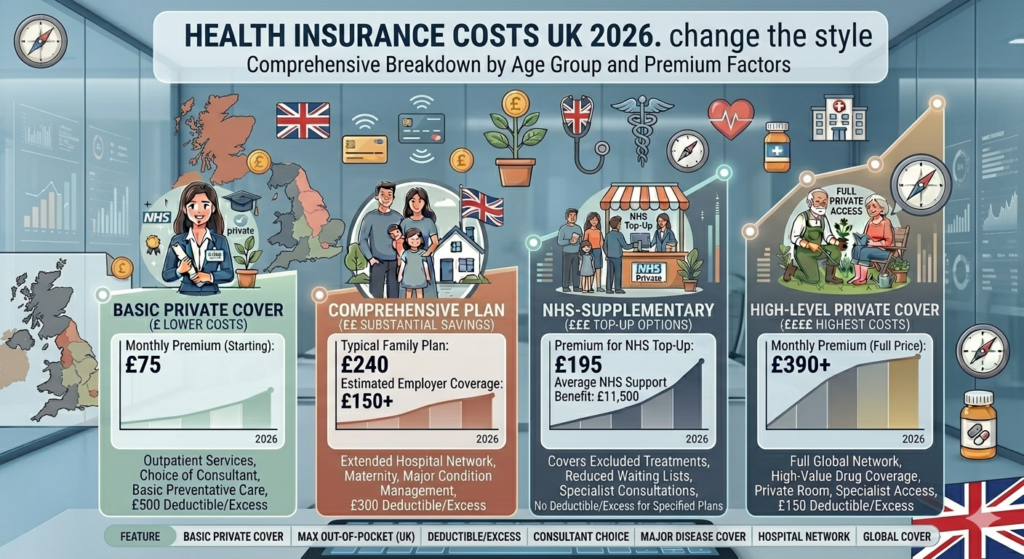

Section 2 – Average Cost of Individual Health Insurance UK (2026)

Nationwide Cost Benchmarks

As of 2026, individual health insurance premiums in the UK vary significantly by age and coverage level. Based on independent research of 12,000+ quotes:

| Age Bracket | Basic Plan (£/month) | Comprehensive Plan (£/month) |

|---|---|---|

| 20‑29 | £28 – £40 | £40 – £60 |

| 30‑39 | £35 – £55 | £50 – £75 |

| 40‑49 | £45 – £70 | £65 – £95 |

| 50‑59 | £60 – £100 | £90 – £140 |

| 60‑69 | £85 – £130 | £120 – £200 |

| 70+ | £130 – £180 | £180 – £300+ |

Figures based on current price intel from UK health insurance analyses.

The national average for a healthy adult individual PMI plan is around £79.59 per month (~£955 annually).

Section 3 – What Factors Affect Individual Health Insurance Cost?

Your monthly or annual premium is not static — it’s personalised around complex risk models used by UK insurers. The following factors significantly affect cost:

⭐ 1. Age — The Most Powerful Cost Driver

Age is the biggest determinant of premium price because older individuals statistically claim more. A 70‑year‑old can pay up to five times more than someone in their 20s simply for the same level of cover.

As you age:

- Premiums rise

- Underwriting risk increases

- Certain coverage exclusions become more common

⭐ 2. Level of Cover Chosen

Insurance plans range from basic inpatient-only to comprehensive suites that include outpatient consultations, scans and therapies.

- Basic PMI: inpatient hospital treatment only

- Mid-level PMI: includes some outpatient diagnostics

- Comprehensive PMI: full cover including consultations, scans and therapies

The richer the coverage, the higher the premium — but you get broader peace of mind.

⭐ 3. Medical Underwriting and Health Profile

Insurers assess your medical history before offering cover:

- Pre‑existing conditions may be excluded or priced higher

- Lifestyle issues (e.g., smoking) increase cost significantly

- Higher BMI or previous claims history can lead to premium hikes

Some providers use moratorium underwriting which waits to cover pre‑existing conditions after a few claim‑free years — this can affect premium too.

⭐ 4. Geography / Postcode Loading

Healthcare costs vary across the UK. Premiums tend to be:

- Highest in London and South East

- Lower in North England, Scotland or Wales

Hospital cost differences directly influence insurance pricing — so your postcode matters.

⭐ 5. Excess / Deductible Level

A higher voluntary excess (the amount you pay when making a claim) lowers your monthly premium. For example:

- £250 excess: lower discount

- £500 – £1000 excess: significant premium reduction

Choosing excess wisely can balance cost and risk.

⭐ 6. Lifestyle Choices (Smoking, Alcohol, etc.)

Smoking can increase premiums by 15–30%, as insurers see smokers as higher risk for claims.

Section 4 – How Much Does It Cost Annually?

Converting monthly payments makes long‑term budgeting clearer:

| Plan Type | Approx Annual Cost |

|---|---|

| Basic PMI | £350 – £850 |

| Mid‑Range PMI | £950 – £1,500 |

| Comprehensive PMI | £1,200 – £2,400+ |

Actual annual cost reflects personal risk factors and policy choices.

Section 5 – Ways to Reduce Individual Health Insurance Costs

If affordability is a concern, careful planning and strategy help:

1. Start Younger

Premiums are cheapest in your 20s and 30s — locking in a policy early saves money over time.

2. Choose Excess Strategically

Agreeing to pay more out of pocket lowers monthly premiums.

3. Restrict Hospital Lists

Limited lists (not all private hospitals) reduce insurer risk and cost.

4. Avoid Add‑Ons You Don’t Need

Skipping dental/optical riders lowers premiums, if your base plan doesn’t require them.

5. Maintain a Healthy Lifestyle

Non‑smokers and those keeping BMI within recommended ranges often pay less.

6. Annual Policy Review

Shop around at renewal — rates can vary between providers.

7. Group/Work Benefits

If available, employer‑provided private health insurance often costs 30–50% less than individual cover.

Section 6 – Typical Coverage vs What’s Not Covered

Typically Covered

- Consultant and specialist fees

- Diagnostic tests (MRI, CT, X‑ray)

- In‑patient and day‑case surgeries

- Some outpatient therapy (if selected)

Not Usually Covered

- Routine GP appointments

- Dental/optical (unless added)

- Chronic condition management

- Pre‑existing condition treatment (often excluded initially)

Understanding these helps set realistic expectations.

Section 7 – Real‑World Cost Examples

Here’s how costs may look in practice:

Example 1: Young Professional (Age 28)

- Mid‑range PMI: ~£40–£60/month

- Annual: ~£480–£720

Example 2: Mid‑Age Adult (Age 45)

- Comprehensive PMI: ~£65–£95/month

- Annual: ~£780–£1,140

Example 3: Near Retirement (Age 65)

- Comprehensive PMI: ~£120–£200/month

- Annual: ~£1,440–£2,400

These figures demonstrate how age and coverage level lead to meaningful cost divergence.

Section 8 – Pros & Cons of Private Health Insurance in the UK

| Pros | Cons |

|---|---|

| Faster access to specialists | Can be more expensive than NHS |

| Choice of hospitals and consultants | Some conditions not covered |

| Avoid NHS waiting lists | Renewal premiums rise with age |

| Optional outpatient cover | Excess costs out of pocket |

| Peace of mind | Add‑ons may increase price |

Balanced decision‑making involves weighing individual needs vs cost.

3. FAQs (Featured Snippet Ready)

1. What is the average cost of individual health insurance in the UK in 2026?

The average cost for an individual private health insurance policy is approximately £79.59 per month (~£955 annually), although this varies significantly by age, cover level and personal factors.

2. How much does age affect UK health insurance premiums?

Age has the most influence — premiums can be 4–5x higher for older adults compared to younger ones due to increased statistical risk of requiring treatment.

3. Can smokers expect to pay more for PMI in the UK?

Yes. Smokers typically pay 15–30% more for the same level of cover due to higher health risk profiles.

4. Does private health insurance cover chronic illnesses?

Standard UK PMI usually focuses on acute conditions and does not cover ongoing management of most chronic illnesses, which remain within NHS care.

5. How can I reduce my individual health insurance cost?

Strategies include choosing higher excess, limiting hospital lists, shopping at renewal, and maintaining a healthy lifestyle.

Disclaimer: The information provided in this article titled ‘individual health insurance cost UK’ is for educational and informational purposes only. While we strive for accuracy and reliability, we recommend verifying details from official sources or professionals before making decisions.

Also read about,