Navigating health insurance can be confusing, especially when terms like deductible, copay, coinsurance, and out-of-pocket maximum appear on your policy. Understanding the health insurance deductible is critical to managing your medical expenses and choosing the right plan.

This guide explains everything about deductibles — what they are, how they work, examples, types, impact on premiums, strategies to reduce costs, and practical tips for 2026.

Introduction – Why Deductibles Matter

A deductible is the amount you pay for covered healthcare services before your insurance starts to pay. Choosing the right deductible affects:

- Monthly premiums: Higher deductibles usually lower monthly premiums.

- Out-of-pocket costs: Lower deductibles mean higher premiums but lower costs when you need care.

- Financial planning: Helps families or individuals plan for potential medical expenses.

For example, if your deductible is $1,500, you pay the first $1,500 of medical bills, then your insurance begins covering costs based on your coinsurance or copay arrangements. (healthcare.gov)

Section 1 – What Is a Health Insurance Deductible?

Definition

A health insurance deductible is the fixed amount an insured person must pay out of pocket for covered medical services before insurance coverage starts paying.

Key Points:

- Deductibles reset annually (usually January 1 in the U.S.).

- Only applies to services covered under your plan.

- Doesn’t include premiums — you always pay those.

Example:

- Deductible: $1,500

- Medical bill: $2,000

- You pay $1,500

- Insurance covers the remaining $500 (subject to coinsurance)

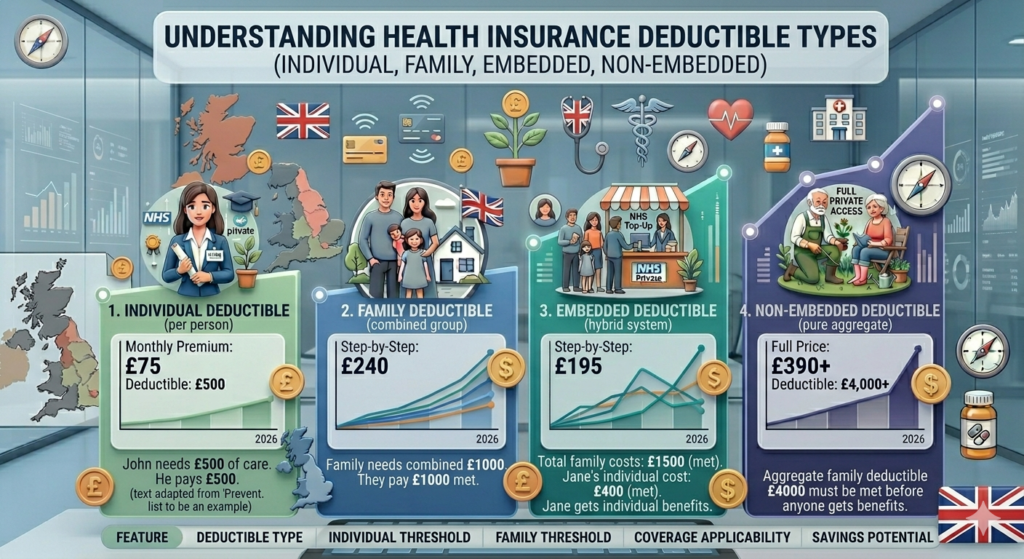

Section 2 – Types of Deductibles

1. Individual Deductible

Applies per person. Common in family plans: each member must meet their own deductible before insurance coverage applies.

2. Family Deductible

Covers the entire family plan. Sometimes, individual deductibles count toward the family deductible. Once the family deductible is met, the plan pays for all members.

3. Embedded Deductible

- Each family member has an individual deductible.

- Once any member meets their deductible, insurance begins paying for that individual, even if the family deductible is not met.

4. Non-Embedded Deductible

- The family deductible must be met in total before insurance pays for anyone.

- Typically used in small family plans.

Section 3 – How Deductibles Work

Deductibles function alongside copayments and coinsurance.

- Copay: Fixed fee per visit (e.g., $30 for a doctor visit).

- Coinsurance: Percentage of costs you pay after the deductible (e.g., 20%).

Example:

- Deductible: $1,500

- Coinsurance: 20%

- Medical bill: $2,500

Calculation:

- Pay $1,500 (deductible)

- Remaining $1,000 x 20% = $200 (coinsurance)

- Insurance pays $800

Section 4 – Deductibles and Premiums

There’s an inverse relationship between deductible and premium:

| Deductible | Monthly Premium | Suitable For |

|---|---|---|

| Low ($500–$1,000) | High | Frequent healthcare users, chronic conditions |

| Medium ($1,500–$2,500) | Moderate | Occasional care, balanced risk |

| High ($3,000–$6,000+) | Low | Healthy individuals, rarely need medical services |

Tip: Consider your expected healthcare use to balance the deductible and premium.

Section 5 – Out-of-Pocket Maximum vs Deductible

The out-of-pocket maximum is different from the deductible:

- Deductible: What you pay before insurance pays

- Out-of-pocket maximum: The most you pay in a year, including deductible, copays, and coinsurance

Example:

- Deductible: $1,500

- Coinsurance: 20%

- Out-of-pocket max: $6,000

If bills exceed $6,000, insurance pays 100% of covered services for the rest of the year.

Section 6 – Strategies to Manage Deductibles

- Choose the Right Plan for Your Needs

- High deductible → lower premiums, but pay more in emergencies

- Low deductible → higher premiums, better coverage for frequent care

- Use Health Savings Accounts (HSA)

- Tax-advantaged account to pay for deductible and medical expenses

- Funds roll over annually

- Plan Medical Expenses

- Schedule elective procedures early in the year to maximize insurance benefits

- Track your deductible progress

- Preventive Care

- Most ACA plans cover preventive services at 100%

- Helps reduce unexpected costs

- Compare Multiple Plans

- Look at total expected annual cost: premiums + deductible + out-of-pocket costs

Section 7 – Deductible Examples (2026)

Scenario 1 – Healthy Individual

- Deductible: $2,500

- Premium: $350/month

- Medical use: Minor check-ups ($300)

- Total annual cost: $4,200 (premium + medical bills)

Scenario 2 – Family of 3

- Deductible: $4,500 family deductible, $1,500 embedded per member

- Premium: $1,200/month

- Medical use: Minor illness + one ER visit ($3,000)

- Total annual cost: $15,000 + $3,000 = $18,000

Scenario 3 – High-Use Plan

- Deductible: $500

- Premium: $600/month

- Multiple specialist visits + imaging (~$5,000)

- Total annual cost: $7,200 + $500 + coinsurance = $7,700–$8,000

Section 8 – Pros and Cons of High vs Low Deductibles

| Deductible Type | Pros | Cons |

|---|---|---|

| High Deductible | Lower premiums, HSA eligible | Higher out-of-pocket if care needed |

| Low Deductible | Predictable costs, better coverage for chronic care | Higher monthly premiums |

Section 9 – Common Questions About Deductibles

1. Does a deductible include copays?

Usually, no. Copays may apply before or after deductible depending on plan design.

2. Are preventive services subject to deductibles?

No, ACA plans cover preventive care at 100% without applying to your deductible.

3. Does a deductible reset annually?

Yes, most plans reset January 1st each year.

4. Can I pay my deductible with HSA funds?

Yes, HSAs are tax-advantaged and can cover deductibles, copays, and coinsurance.

5. What happens if I don’t meet my deductible?

You pay full cost for medical services up to the deductible. Insurance coverage begins after meeting it.

Section 10 – Practical Tips

- Track your deductible online with insurer portals

- Budget for your deductible at the start of the year

- Consider high-deductible plans with HSA if healthy

- Review plan annually to ensure it fits your expected medical needs

Disclaimer: The information provided in this article titled ‘health insurance deductible explanation’ is for educational and informational purposes only. While we strive for accuracy and reliability, we recommend verifying details from official sources or professionals before making decisions.

Also read about,