Choosing the right health insurance plan can be overwhelming. With multiple coverage options, premium ranges, deductibles, and out-of-pocket costs, comparing prices is essential for smart financial planning. This guide will show how to compare health insurance prices effectively, understand what affects costs, and pick the best plan for your needs in 2026.

Introduction – Why Comparing Health Insurance Prices Matters

Health insurance is one of the largest recurring expenses for individuals and families in the United States. A slight difference in premiums, deductibles, or coinsurance can result in thousands of dollars in annual savings. Conducting a thorough price comparison ensures you get optimal coverage at a reasonable cost.

Section 1 – Types of Health Insurance Plans

When comparing prices, it’s important to understand the types of plans available:

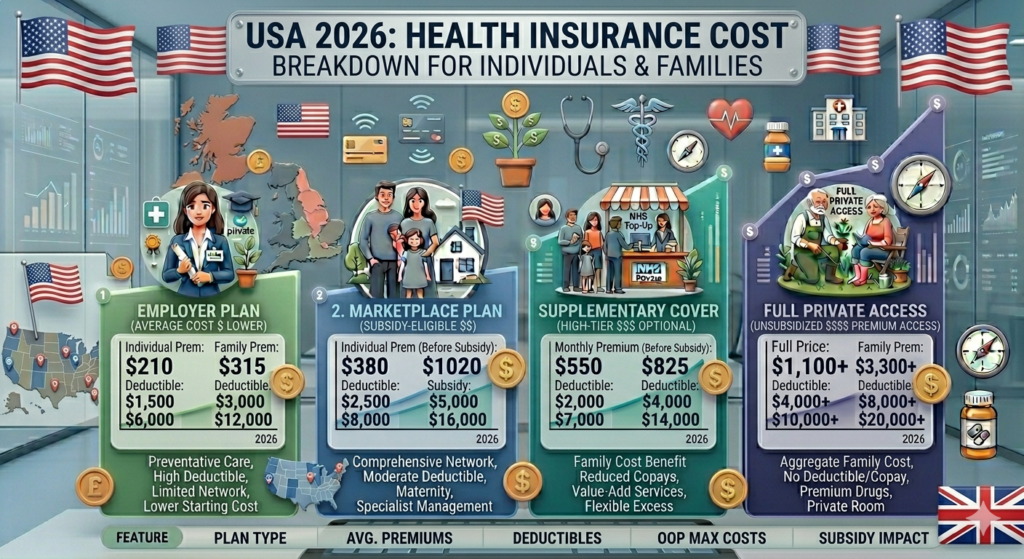

1. Employer-Sponsored Insurance (ESI)

- Offered through employers

- Premiums partially covered by employer

- Typically includes family plans and benefits like dental/vision

- Usually lower cost for employees than private plans

2. Marketplace / ACA Plans

- Purchased through Healthcare.gov or state exchanges

- Four metal tiers: Bronze, Silver, Gold, Platinum

- Subsidies available for eligible families based on income

- Premiums vary by state and tier

3. Private Insurance Plans

- Purchased directly from insurance companies

- Flexible coverage and provider networks

- Premiums typically higher without subsidies

- Good option for high-income families or those not eligible for ACA subsidies

Section 2 – Factors Affecting Health Insurance Prices

Premiums differ based on multiple variables:

- Age: Older adults pay higher premiums; ACA limits to 3x age factor

- Location: States and regions with higher healthcare costs have higher premiums

- Plan Type: Metal tier, coverage network, and included benefits affect price

- Family Size: Family coverage is significantly higher than individual coverage

- Income & Subsidies: ACA tax credits reduce premiums for eligible households

- Health Risk: Pre-ACA private plans often priced based on medical history

Section 3 – How to Compare Health Insurance Prices

Step 1 – Identify Your Needs

- Individual vs family coverage

- Expected medical usage (chronic conditions, prescriptions)

- Preferred network of doctors and hospitals

Step 2 – Check Multiple Sources

- Employer-sponsored plans

- ACA Marketplace plans (Healthcare.gov or state exchange)

- Private insurance companies

Step 3 – Compare Key Cost Metrics

- Monthly premiums

- Deductibles

- Copays and coinsurance

- Out-of-pocket maximums

- Coverage for prescriptions, dental, vision, and preventive care

Step 4 – Include Tax Credits / Employer Contributions

- ACA subsidies reduce premiums for qualifying families

- Employer contributions lower out-of-pocket costs for ESI

Section 4 – Price Comparison Examples (2026)

| Plan Type | Family Premium (Monthly) | Deductible | Out-of-Pocket Max | Notes |

|---|---|---|---|---|

| Employer-sponsored | $550–$700 | $1,500 | $6,000 | Employer covers 65–75% of cost |

| ACA Marketplace Bronze | $850–$1,050 | $3,500 | $9,000 | Subsidy lowers cost for eligible families |

| ACA Marketplace Silver | $1,050–$1,300 | $2,500 | $7,000 | Most balanced coverage for families |

| Private Direct | $900–$1,400 | $2,000 | $6,500 | Flexible provider networks, no subsidy |

Section 5 – Comparing Premium vs Deductible Trade-Off

Higher premiums usually mean lower deductibles, and vice versa:

- Low premium / high deductible: Ideal for healthy individuals, low medical usage

- High premium / low deductible: Ideal for chronic conditions or frequent care

Example Calculation:

- Plan A: $400/month, $3,000 deductible → Annual cost if medical bills $2,000 = $4,800 (premium) + $2,000 = $6,800

- Plan B: $700/month, $1,000 deductible → Annual cost = $8,400 (premium) + $1,000 = $9,400

Even though Plan B has a higher premium, it may save money if medical expenses are frequent.

Section 6 – Tools and Websites for Price Comparison

- Healthcare.gov – official Marketplace plans and subsidies

- State Exchanges – some states have their own comparison tools

- Insurance Company Websites – for private plans

- Employer HR Portals – comparison of employee-sponsored plans

- Third-Party Aggregators – e.g., eHealthInsurance, Policygenius

Section 7 – Tips to Save Money on Health Insurance

- Use Tax Credits and Subsidies: Maximize ACA assistance

- Select High-Deductible Plans (with HSA): Reduces monthly premium, allows tax-free savings

- Evaluate Employer Contributions: Choose plans with employer contribution to premiums or HSA

- Stay In-Network: Avoid out-of-network costs

- Annual Plan Review: Compare costs every year; premiums change annually

Section 8 – Common Mistakes When Comparing Prices

- Focusing only on monthly premium and ignoring deductible

- Not checking copays and coinsurance

- Overlooking out-of-pocket maximums

- Forgetting prescription and specialty coverage

- Ignoring network restrictions

Section 9 – Real-World Scenario (Family of 4 – 2026)

- Family needs: 2 adults, 2 children, moderate medical use

- Employer Plan: $600/month, $1,500 deductible → Total expected annual cost: ~$9,000

- Marketplace Silver: $1,200/month, $2,500 deductible → Subsidy reduces monthly to $400 → Total: ~$6,300

- Private Plan: $1,100/month, $2,000 deductible → No subsidy → Total: ~$15,200

Lesson: Price comparison considering subsidies and expected medical costs is critical.

Section 10 – FAQs (Featured Snippet Optimized)

1. How can I compare health insurance prices effectively?

Compare monthly premiums, deductibles, copays, coinsurance, out-of-pocket maximums, and coverage benefits across multiple sources.

2. Are Marketplace plans cheaper than private insurance?

They can be, especially with ACA subsidies for eligible families.

3. Does employer-sponsored insurance always cost less?

Usually, because employers contribute to premiums, but options may be limited.

4. Should I prioritize premiums or out-of-pocket costs?

Balance based on expected medical usage. High-use families benefit from low deductibles; low-use individuals can save with lower premiums.

5. Can I switch plans mid-year for cost reasons?

Generally, only during open enrollment or qualifying life events like marriage, birth, or job change.

Disclaimer: The information provided in this article titled ‘health insurance price comparison’ is for educational and informational purposes only. While we strive for accuracy and reliability, we recommend verifying details from official sources or professionals before making decisions.

Also read about

Average Monthly Health Insurance Premium – 2026 Complete Guide