Being self-employed in the United States offers freedom, flexibility, and control over your income. But it also comes with one major responsibility — managing your own health insurance.

Unlike traditional employees, freelancers, gig workers, and small business owners don’t have employer-sponsored health coverage. This means you must find, compare, and pay for your own plan.

The good news? There are multiple affordable and flexible options available.

In this complete guide, you’ll learn everything about health insurance for self-employed USA, including costs, plan types, tax benefits, and how to choose the best coverage.

Why Health Insurance Matters for the Self-Employed

Health insurance is not just a legal or financial decision. It’s protection against unexpected medical costs.

A single hospital visit in the U.S. can cost thousands of dollars. Without insurance, this can severely impact your finances.

Key reasons to get coverage:

- Protection from high medical bills

- Access to preventive care

- Financial stability during emergencies

- Compliance with healthcare standards (in some states)

Even if you’re healthy, insurance is essential for long-term security.

Who Qualifies as Self-Employed?

You are considered self-employed if you:

- Work as a freelancer or contractor

- Run your own business

- Earn gig income (Uber, Fiverr, Upwork, etc.)

- Have no employer-sponsored insurance

This category includes millions of Americans today.

Types of Health Insurance for Self-Employed Individuals

Understanding your options is the first step toward choosing the right plan.

1. ACA Marketplace Plans (HealthCare.gov)

These are the most common and recommended options.

Features:

- Available through federal or state exchanges

- Covers essential health benefits

- Offers subsidies based on income

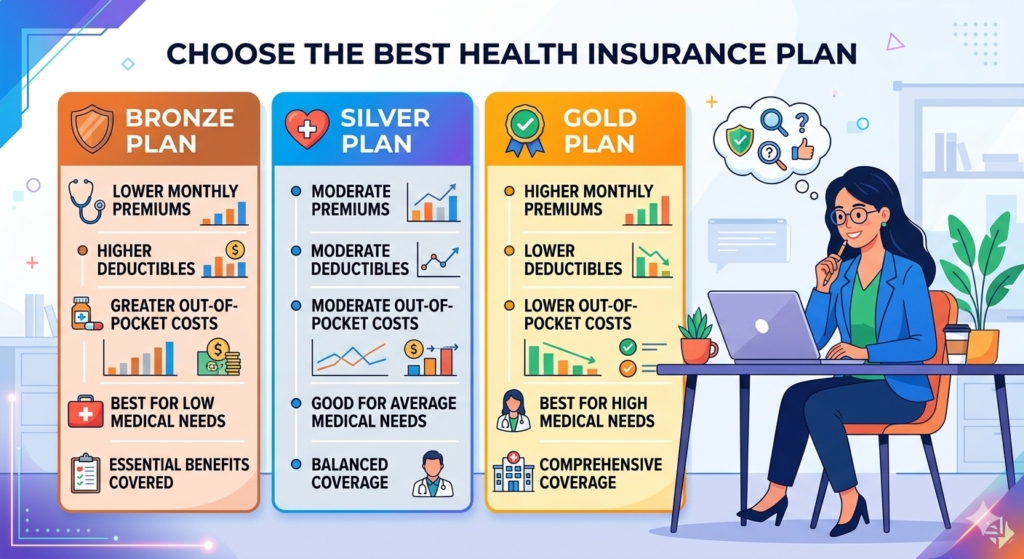

Plan Categories:

- Bronze (lowest premium, high deductible)

- Silver (balanced option)

- Gold (higher premium, lower costs)

- Platinum (highest premium, lowest out-of-pocket)

Best for: Individuals with moderate income who qualify for subsidies.

2. Private Health Insurance Plans

You can buy plans directly from insurance companies.

Pros:

- More customization

- Wider network options

Cons:

- No government subsidies

- Can be more expensive

3. Short-Term Health Insurance

Temporary coverage for limited periods.

Key points:

- Lower monthly premiums

- Limited coverage

- May not cover pre-existing conditions

Best for: People between jobs or waiting for enrollment.

4. Health Sharing Plans

Not traditional insurance. Members share medical costs.

Pros:

- Lower monthly cost

- Flexible participation

Cons:

- Not regulated like insurance

- Limited coverage guarantees

5. COBRA Coverage

If you recently left a job, you can continue your employer’s plan.

Important:

- Expensive (you pay full premium)

- Temporary (usually up to 18 months)

How Much Does Health Insurance Cost for Self-Employed?

Costs vary widely depending on several factors.

Key cost factors:

- Age

- Location

- Income

- Plan type

- Coverage level

Typical monthly premiums (approximate ranges):

- Individual: $300 – $700

- Family: $800 – $1,500+

These are general estimates and can vary significantly.

How to Lower Your Health Insurance Costs

Healthcare can be expensive, but there are smart ways to save.

1. Use Premium Tax Credits

If your income falls within a certain range, you qualify for subsidies.

2. Choose a High Deductible Plan (HDHP)

Lower monthly premium but higher out-of-pocket costs.

3. Open a Health Savings Account (HSA)

Tax-advantaged account for medical expenses.

4. Compare Plans Annually

Prices and coverage change every year.

5. Bundle Family Coverage

Sometimes family plans are more cost-effective.

Tax Benefits for Self-Employed Health Insurance

One of the biggest advantages is tax deductions.

Self-Employed Health Insurance Deduction

You can deduct:

- Health insurance premiums

- Dental insurance

- Long-term care insurance

This reduces your taxable income.

HSA Tax Benefits

- Contributions are tax-deductible

- Growth is tax-free

- Withdrawals for medical expenses are tax-free

Best Health Insurance Providers for Self-Employed (USA)

Some well-known insurers include:

- Blue Cross Blue Shield

- UnitedHealthcare

- Aetna

- Cigna

- Kaiser Permanente

Each provider offers different plans and network coverage.

How to Choose the Right Plan

Choosing the right plan requires careful analysis.

Step-by-step guide:

1. Evaluate Your Health Needs

- Do you visit doctors often?

- Do you take regular medications?

2. Set a Budget

Balance between premium and deductible.

3. Check Provider Networks

Ensure your doctor is included.

4. Compare Out-of-Pocket Costs

Includes:

- Deductibles

- Copayments

- Coinsurance

5. Review Coverage Benefits

Look for:

- Preventive care

- Emergency services

- Prescription coverage

Common Mistakes to Avoid

Many self-employed individuals make costly mistakes.

Avoid these errors:

- Choosing the cheapest plan without checking coverage

- Ignoring deductibles and out-of-pocket limits

- Not checking provider networks

- Skipping insurance altogether

Open Enrollment and Special Enrollment Periods

Open Enrollment:

Usually runs from November to January.

Special Enrollment:

Triggered by life events:

- Marriage

- Birth of a child

- Loss of other coverage

Missing enrollment deadlines can leave you uninsured.

Health Insurance for Freelancers vs Small Business Owners

Freelancers:

- Typically use individual marketplace plans

Small Business Owners:

- May qualify for group health insurance

- Can offer employee benefits

Is Health Insurance Mandatory for Self-Employed?

There is no federal penalty for not having insurance. However:

- Some states impose penalties

- Medical costs without insurance can be overwhelming

Best Strategies for Long-Term Coverage

To ensure stability:

- Review plans annually

- Adjust coverage based on income

- Maintain an emergency health fund

- Use preventive healthcare services

Future Trends in Self-Employed Health Insurance

Healthcare is evolving rapidly.

Key trends:

- Telehealth services

- Digital insurance platforms

- Personalized coverage plans

- AI-driven healthcare recommendations

Conclusion

Finding the right health insurance for self-employed USA is essential for financial security and peace of mind.

While it may seem complex, understanding your options simplifies the process. Whether you choose an ACA plan, private insurance, or a high-deductible plan with an HSA, the key is to match coverage with your needs and budget.

Take time to compare plans, use available tax benefits, and review your coverage every year.

Your health is your most valuable asset — protect it wisely.

3. FAQs (Featured Snippet Optimized)

1. What is the best health insurance for self-employed individuals in the USA?

The best option is usually an ACA Marketplace plan because it offers comprehensive coverage and income-based subsidies.

2. Can self-employed people get health insurance tax deductions?

Yes, self-employed individuals can deduct health insurance premiums from their taxable income.

3. How much does health insurance cost for self-employed?

Costs typically range from $300 to $700 per month for individuals, depending on coverage and location.

4. Is it cheaper to buy private health insurance or marketplace plans?

Marketplace plans are often cheaper due to subsidies, especially for low to moderate-income individuals.

5. What happens if a self-employed person has no health insurance?

They must pay all medical expenses out-of-pocket, which can be extremely costly.

Disclaimer: The information provided in this article titled ‘health insurance for self-employed USA’ is for educational and informational purposes only. While we strive for accuracy and reliability, we recommend verifying details from official sources or professionals before making decisions.

Also read about,