Running a small business in the United States is challenging. You manage operations, employees, and growth — all while keeping costs under control.

One of the biggest decisions you will make is offering health insurance to your employees.

Health insurance is not just a benefit. It is a powerful tool to attract talent, retain employees, and improve productivity.

But many business owners ask the same question:

How can I find affordable health insurance for my small business?

In this complete guide, you’ll learn everything about health insurance for small businesses, including plan types, costs, tax credits, and strategies to save money.

What is Considered a Small Business?

In the U.S., a small business is typically defined as having:

- Fewer than 50 full-time employees (FTEs)

- Some states extend this up to 100 employees

If your business falls in this range, you qualify for small group health insurance plans.

Why Health Insurance Matters for Small Businesses

Offering health insurance is a strategic investment.

Key benefits:

- Attract and retain top talent

- Increase employee satisfaction

- Improve productivity

- Reduce absenteeism

- Gain tax advantages

In a competitive job market, benefits often matter as much as salary.

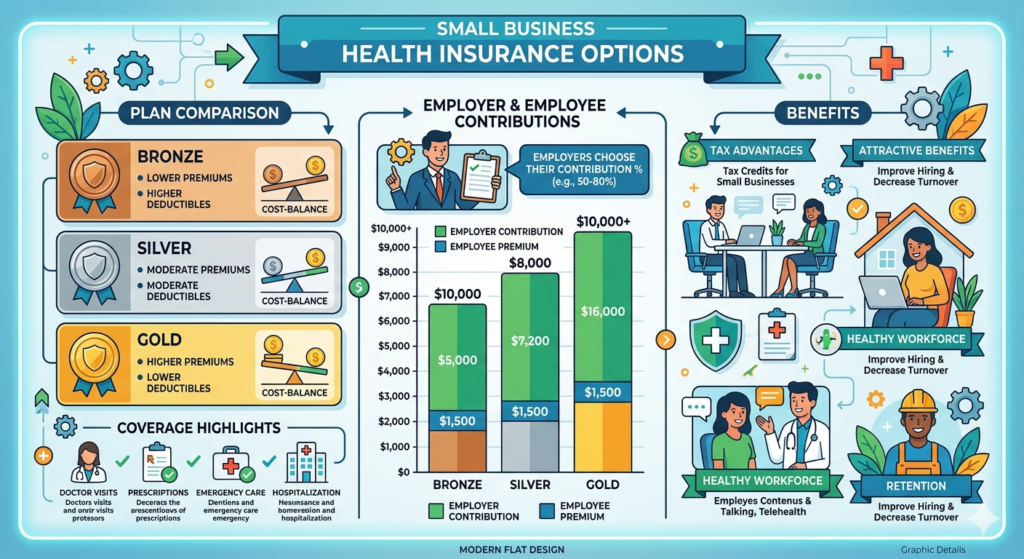

Types of Health Insurance for Small Businesses

Understanding your options helps you choose wisely.

1. Small Group Health Insurance Plans

These are traditional employer-sponsored plans.

Features:

- Covers employees and dependents

- Shared cost between employer and employees

- Comprehensive coverage

Best for:

Businesses with 1–50 employees looking for structured plans.

2. SHOP Marketplace Plans

SHOP (Small Business Health Options Program) is a government platform.

Advantages:

- Access to tax credits

- Multiple plan choices

- Regulated and standardized

Requirements:

- Fewer than 25 employees (for tax credit eligibility)

- Meet contribution and participation rules

3. Health Reimbursement Arrangements (HRAs)

Employers reimburse employees for medical expenses.

Popular options:

- QSEHRA (Qualified Small Employer HRA)

- ICHRA (Individual Coverage HRA)

Benefits:

- Cost control

- Flexibility

- Employees choose their own plans

4. Self-Funded (Level-Funded) Plans

Employer assumes some financial risk.

Pros:

- Potential cost savings

- Customizable coverage

Cons:

- Financial risk if claims are high

5. Association Health Plans (AHPs)

Small businesses join together to get better rates.

Benefits:

- Lower premiums

- Larger risk pool

How Much Does Small Business Health Insurance Cost?

Costs depend on multiple factors.

Key factors:

- Number of employees

- Employee age

- Location

- Coverage level

- Plan type

Average employer costs:

- Single coverage: $400 – $800/month per employee

- Family coverage: $1,000 – $2,000+/month

Employers typically pay 50% to 70% of premiums.

Small Business Health Care Tax Credit

One of the biggest advantages of offering insurance.

Eligibility:

- Fewer than 25 full-time employees

- Average wages below a set threshold

- Employer pays at least 50% of premiums

Benefit:

- Up to 50% tax credit on premium costs

This significantly reduces overall expenses.

How to Choose the Right Plan for Your Business

Making the right decision requires careful planning.

Step-by-step approach:

1. Assess Your Budget

Decide how much your business can contribute.

2. Understand Employee Needs

- Age group

- Family size

- Healthcare usage

3. Compare Plan Types

Evaluate:

- Premiums

- Deductibles

- Networks

4. Check Provider Networks

Ensure access to quality healthcare providers.

5. Work with a Broker

Insurance brokers can simplify the process.

Key Features to Look For in a Plan

Essential benefits:

- Preventive care

- Emergency services

- Prescription drugs

- Mental health services

- Maternity care

Pros and Cons of Offering Health Insurance

Pros:

- Stronger employee retention

- Tax benefits

- Competitive advantage

Cons:

- High costs

- Administrative complexity

- Compliance requirements

How to Reduce Health Insurance Costs

Small businesses can control costs with smart strategies.

1. Offer High Deductible Health Plans (HDHPs)

Lower premiums for employers.

2. Use HRAs

Control reimbursement limits.

3. Promote Wellness Programs

Healthier employees = lower claims.

4. Compare Plans Annually

Switch to better options when needed.

5. Adjust Employer Contribution

Balance between affordability and coverage.

Compliance and Legal Requirements

Affordable Care Act (ACA):

- Businesses with 50+ employees must offer insurance

- Smaller businesses are not required but encouraged

State Laws:

Some states have additional requirements.

Best Health Insurance Providers for Small Businesses

Top providers include:

- Blue Cross Blue Shield

- UnitedHealthcare

- Aetna

- Cigna

- Kaiser Permanente

Each offers different plans and network coverage.

Common Mistakes to Avoid

Avoid these pitfalls:

- Choosing the cheapest plan without evaluating coverage

- Ignoring employee needs

- Not reviewing plans annually

- Failing to understand tax benefits

Health Insurance vs Salary: What Employees Prefer

Many employees prefer benefits over higher salaries.

Why?

- Healthcare costs are unpredictable

- Insurance provides security

- Tax advantages for employees

Future Trends in Small Business Health Insurance

Emerging trends:

- Telehealth integration

- AI-driven plan selection

- Personalized coverage

- Digital health platforms

Conclusion

Offering health insurance for small businesses is one of the smartest investments you can make.

It helps attract talent, improves employee satisfaction, and provides tax advantages.

While costs can be high, options like SHOP plans, HRAs, and tax credits make it more affordable than ever.

The key is to evaluate your business needs, compare plans carefully, and choose a solution that balances cost and coverage.

3. FAQs (Featured Snippet Optimized)

1. Do small businesses have to provide health insurance?

No, businesses with fewer than 50 employees are not required, but offering insurance provides benefits and tax advantages.

2. What is the cheapest health insurance option for small businesses?

HRAs and SHOP marketplace plans are often the most affordable options.

3. How much do small businesses pay for health insurance?

Employers typically pay $400–$800 per employee monthly for individual coverage.

4. What is the SHOP marketplace?

SHOP is a government platform where small businesses can purchase group health insurance and access tax credits.

5. Can a small business get tax credits for health insurance?

Yes, eligible businesses can receive up to 50% tax credit on premium costs.

Disclaimer: The information provided in this article titled ‘health insurance for small businesses’ is for educational and informational purposes only. While we strive for accuracy and reliability, we recommend verifying details from official sources or professionals before making decisions.

Also read about,