Freelancing in the UK offers flexibility, independence, and control over your income. But it also comes with one major responsibility — managing your healthcare.

Unlike employees, freelancers don’t receive employer-sponsored benefits. While the NHS provides free healthcare, many freelancers are now exploring private health insurance.

Why?

Because time is money.

Long waiting times, delayed treatments, and lack of sick pay can directly impact your income.

In this complete guide, you’ll learn everything about health insurance for freelancers UK, including options, costs, benefits, and how to choose the right plan.

Do Freelancers Need Health Insurance in the UK?

The UK has the National Health Service (NHS), which provides free healthcare at the point of use.

So technically, you don’t need private insurance.

However, many freelancers still choose it.

Why?

- Faster access to treatment

- Avoid NHS waiting lists

- Flexible appointment times

- Access to private hospitals

Private health insurance allows you to bypass delays and get quicker diagnosis and treatment.

For freelancers, this means less downtime and quicker return to work.

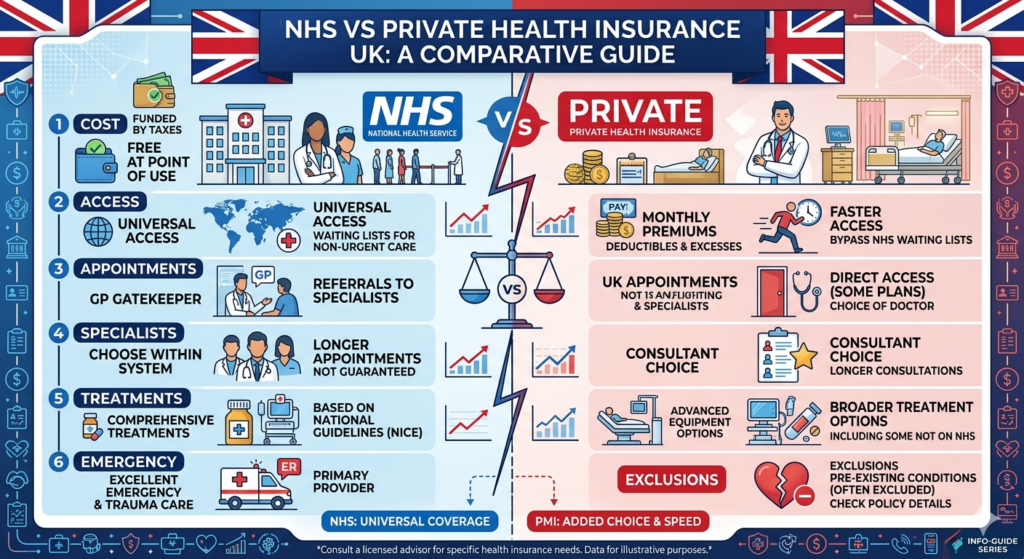

NHS vs Private Health Insurance: Key Differences

NHS (Public Healthcare)

- Free for UK residents

- Covers most treatments

- Longer waiting times for non-urgent care

Private Health Insurance

- Paid monthly or annually

- Faster access to specialists

- More control over treatment timing

Private insurance works alongside the NHS, not as a replacement.

What is Health Insurance for Freelancers?

Health insurance for freelancers is simply private medical insurance (PMI) tailored to individuals.

It covers the cost of:

- Private consultations

- Diagnostic tests

- Surgery and treatment

- Hospital stays

Most freelancers purchase personal policies, not business ones.

What Does Freelancer Health Insurance Cover?

Coverage depends on your plan.

Common inclusions:

- Specialist consultations

- Diagnostic tests (MRI, CT scans)

- Surgery and hospital treatment

- Cancer care

- Mental health support

- Physiotherapy

Many insurers also offer online GP services and 24/7 support.

What is NOT Covered?

Most policies exclude:

- Pre-existing conditions (initially)

- Chronic illnesses (like diabetes)

- Routine GP visits (in basic plans)

Private insurance mainly focuses on acute conditions that can be treated and resolved.

Types of Health Insurance for Freelancers UK

1. Basic Private Health Insurance

Features:

- Covers major treatments and hospital stays

- Lower monthly premium

Best for: Budget-conscious freelancers.

2. Comprehensive Health Insurance

Includes:

- Outpatient care

- Diagnostics

- Specialist consultations

Best for: Freelancers who want full protection.

3. Modular / Custom Plans

Flexible plans where you choose coverage options.

Options include:

- Dental and optical cover

- Therapies (physio, chiropractic)

- Mental health services

This flexibility allows freelancers to control costs.

4. Income Protection Insurance (Add-On)

Not health insurance, but highly relevant.

Covers:

- Loss of income due to illness

Important because freelancers usually don’t receive sick pay.

How Much Does Health Insurance Cost in the UK?

Costs vary depending on several factors.

Typical monthly cost:

- Basic plans: £50 – £150

- Mid-range plans: £150 – £300

- Comprehensive plans: £300 – £500+

Factors affecting cost:

- Age

- Location (London is more expensive)

- Lifestyle (smoking, BMI)

- Level of cover

- Excess amount

Choosing a higher excess lowers your premium.

Is Health Insurance Tax Deductible for Freelancers UK?

This is an important point.

For sole traders:

- Health insurance is considered a personal expense

- It is not tax-deductible

For limited companies:

- Can sometimes be treated as a business expense

- May have tax implications

Always consult an accountant for accurate advice.

Best Health Insurance Providers for Freelancers UK

Top insurers include:

- Bupa

- AXA Health

- Vitality Health

- Aviva

- WPA

These providers offer flexible plans designed for individuals and freelancers.

How to Choose the Right Health Insurance Plan

Choosing the right plan requires strategy.

Step-by-step guide:

1. Assess Your Needs

- Do you need fast access to specialists?

- Do you want mental health coverage?

2. Set Your Budget

Balance between:

- Monthly premium

- Out-of-pocket costs

3. Compare Coverage Levels

Look at:

- Inpatient vs outpatient cover

- Diagnostic tests included

4. Check Hospital Networks

Ensure access to nearby private hospitals.

5. Choose the Right Excess

Higher excess = lower premium.

Pros and Cons of Health Insurance for Freelancers

Pros:

- Faster treatment

- Reduced downtime

- Better control over healthcare

- Access to private facilities

Cons:

- Monthly cost

- Doesn’t cover all conditions

- Not tax-deductible (for most freelancers)

Common Mistakes to Avoid

Avoid these costly mistakes:

- Choosing the cheapest plan only

- Ignoring exclusions

- Not checking hospital networks

- Skipping insurance entirely

Real-World Insight (From Freelancers)

Many freelancers view health insurance as a business protection tool.

From community discussions:

“Your health is your income… waiting months can mean lost clients.”

Freelancers often choose private insurance to protect earnings and avoid long NHS delays.

How to Reduce Health Insurance Costs

1. Increase Your Excess

Lower premiums significantly.

2. Limit Outpatient Cover

Reduces monthly cost.

3. Stay Healthy

Lifestyle affects pricing.

4. Compare Quotes Annually

Prices change every year.

Future Trends in UK Freelancer Health Insurance

Emerging trends:

- Digital GP services

- Telehealth consultations

- AI-driven insurance pricing

- Personalized health plans

Conclusion

Choosing the right health insurance for freelancers UK is about balancing cost, coverage, and convenience.

While the NHS provides essential care, private insurance offers speed, flexibility, and peace of mind — especially for freelancers whose income depends on staying healthy.

If you rely on your work for income, investing in health insurance is not just a personal decision — it’s a business decision.

Take time to compare plans, understand your needs, and choose wisely.

3. FAQs (Featured Snippet Optimized)

1. Do freelancers need health insurance in the UK?

No, the NHS provides free healthcare, but private insurance offers faster treatment and more flexibility.

2. How much does health insurance cost for freelancers UK?

Costs typically range from £50 to £500 per month depending on coverage and personal factors.

3. Is private health insurance worth it for freelancers?

Yes, especially if you want quicker access to treatment and want to avoid long NHS waiting times.

4. Can freelancers claim health insurance as a business expense?

Usually no for sole traders, as it is considered a personal expense.

5. What is the best health insurance provider for freelancers UK?

Top providers include Bupa, AXA Health, Vitality, Aviva, and WPA.

Disclaimer: The information provided in this article titled ‘health insurance for freelancers UK’ is for educational and informational purposes only. While we strive for accuracy and reliability, we recommend verifying details from official sources or professionals before making decisions.

Also read about