Turning 65 is a major milestone — especially in the United States. It marks eligibility for Medicare, the primary health insurance program for seniors.

But here’s the reality:

Medicare is not completely free, and it does not cover everything.

Many seniors find themselves confused about:

- What Medicare covers

- Whether they need additional insurance

- How much it will cost

Choosing the right coverage is essential to avoid high out-of-pocket medical expenses.

In this complete guide, you’ll learn everything about health insurance for seniors over 65, including Medicare plans, supplemental coverage, costs, and how to choose the best option.

Why Health Insurance is Critical After Age 65

Healthcare needs increase significantly with age.

Common health needs include:

- Regular doctor visits

- Prescription medications

- Chronic disease management

- Hospital care

Without proper insurance, these costs can quickly become overwhelming.

Understanding Medicare: The Foundation of Senior Health Insurance

Medicare is the primary health insurance program for people aged 65 and older.

It is divided into different parts.

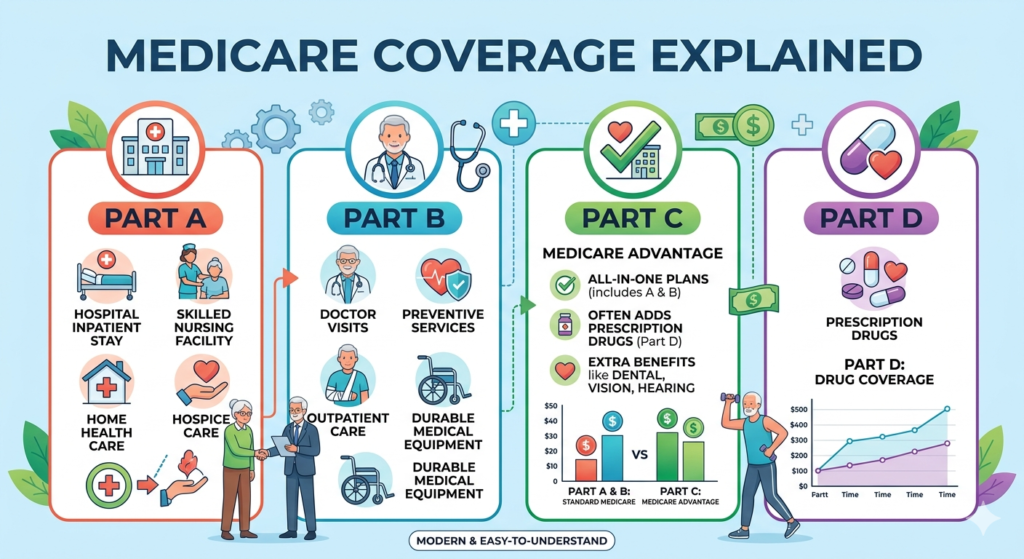

Medicare Part A (Hospital Insurance)

Covers:

- Inpatient hospital stays

- Skilled nursing facility care

- Hospice care

Cost:

- Usually free if you paid Medicare taxes for at least 10 years

Medicare Part B (Medical Insurance)

Covers:

- Doctor visits

- Outpatient services

- Preventive care

Cost:

- Monthly premium (standard amount set annually)

Medicare Part C (Medicare Advantage)

Offered by private insurance companies.

Includes:

- Part A + Part B

- Often includes extra benefits like:

- Dental

- Vision

- Hearing

Key advantage:

All-in-one plan.

Medicare Part D (Prescription Drug Coverage)

Covers:

- Prescription medications

Important:

You must enroll separately if not included in your plan.

What Medicare Does NOT Cover

Many seniors are surprised by gaps in coverage.

Common exclusions:

- Long-term care

- Dental and vision (in Original Medicare)

- Hearing aids

- Overseas medical care

This is why additional coverage is often necessary.

Medigap (Medicare Supplement Insurance)

Medigap helps cover out-of-pocket costs.

Covers:

- Copayments

- Coinsurance

- Deductibles

Benefits:

- Predictable healthcare costs

- Freedom to choose providers

Medicare Advantage vs Medigap: Key Differences

Medicare Advantage:

- Lower premiums

- Network restrictions

- Extra benefits

Medigap:

- Higher premiums

- More flexibility

- Lower out-of-pocket costs

How Much Does Health Insurance Cost After 65?

Costs depend on the plan.

Typical expenses:

- Medicare Part B premium: Standard monthly cost

- Medicare Advantage: $0 – $100+

- Medigap: $100 – $300+

- Part D: $10 – $80+

Factors That Affect Costs

- Income level

- Location

- Plan type

- Coverage level

Higher-income individuals may pay higher premiums.

How to Choose the Right Health Insurance Plan

Step-by-step guide:

1. Decide Between Original Medicare and Advantage

Choose based on flexibility vs cost.

2. Evaluate Your Health Needs

- Do you need frequent care?

- Do you take medications regularly?

3. Check Prescription Drug Coverage

Ensure your medications are covered.

4. Compare Total Costs

Look beyond premiums:

- Deductibles

- Copays

- Out-of-pocket limits

5. Review Provider Networks

Ensure your doctors are included.

Best Health Insurance Providers for Seniors

Top providers include:

- UnitedHealthcare

- Humana

- Aetna

- Blue Cross Blue Shield

- Kaiser Permanente

Enrollment Periods You Must Know

Initial Enrollment Period (IEP):

- Starts 3 months before turning 65

- Ends 3 months after

Annual Enrollment Period (AEP):

- October 15 to December 7

- Change plans

Medicare Advantage Open Enrollment:

- January 1 to March 31

Common Mistakes Seniors Make

Avoid these mistakes:

- Delaying enrollment (can cause penalties)

- Ignoring prescription drug coverage

- Choosing plans based only on premiums

- Not reviewing plans annually

Low-Income Assistance Programs

Available programs:

- Medicaid (for dual eligibility)

- Medicare Savings Programs

- Extra Help (for prescription drugs)

These programs reduce costs significantly.

Health Insurance for Seniors Living Abroad

Medicare generally does not cover care outside the U.S.

Options:

- Travel insurance

- International health insurance

Tips to Reduce Healthcare Costs After 65

1. Use Preventive Services

Many are free under Medicare.

2. Choose In-Network Providers

Reduces costs.

3. Review Plans Annually

Switch if needed.

4. Apply for Assistance Programs

Lower your expenses.

Future Trends in Senior Health Insurance

Emerging trends:

- Telehealth services

- Home-based healthcare

- AI-driven diagnostics

- Personalized Medicare plans

Conclusion

Choosing the right health insurance for seniors over 65 is essential for maintaining your health and financial stability.

Medicare provides a strong foundation, but understanding its limitations is key. Whether you choose Medicare Advantage, Medigap, or additional coverage, the goal is to balance cost and care.

Take time to compare plans, review your needs, and enroll on time.

Your health deserves the best protection — especially in your golden years.

3. FAQs (Featured Snippet Optimized)

1. What is the best health insurance for seniors over 65?

Medicare is the primary option, often combined with Medicare Advantage or Medigap for additional coverage.

2. Is Medicare free after age 65?

Part A is usually free, but Part B and other plans require monthly premiums.

3. What does Medicare not cover?

It does not cover long-term care, dental, vision, or hearing in most cases.

4. Should I choose Medicare Advantage or Medigap?

Choose Advantage for lower premiums and Medigap for flexibility and lower out-of-pocket costs.

5. Can seniors get additional financial help?

Yes, programs like Medicaid and ExtraHelp can reduce costs.

Disclaimer: The information provided in this article titled ‘health insurance for seniors over 65’ is for educational and informational purposes only. While we strive for accuracy and reliability, we recommend verifying details from official sources or professionals before making decisions.

Also read about the,