Turning 50 is a major milestone. It often comes with new priorities — especially when it comes to health.

Medical needs tend to increase with age. Preventive care, regular checkups, and managing chronic conditions become more important. At the same time, health insurance costs also begin to rise.

If you’re self-employed, retired early, or not covered by an employer, finding the right plan can feel overwhelming.

The good news? There are multiple options available.

In this complete guide, you’ll learn everything about health insurance after age 50, including plan types, costs, Medicare eligibility, and smart ways to save money.

Why Health Insurance is Crucial After Age 50

Healthcare becomes more important as you age.

Key reasons to have coverage:

- Increased risk of chronic conditions

- Higher medical expenses

- Need for preventive screenings

- Financial protection from emergencies

Even routine care can become expensive without insurance.

Health Risks and Coverage Needs After 50

People over 50 often require the following:

- Regular health screenings (blood pressure, cholesterol)

- Cancer screenings

- Prescription medications

- Specialist visits

This makes comprehensive health insurance essential.

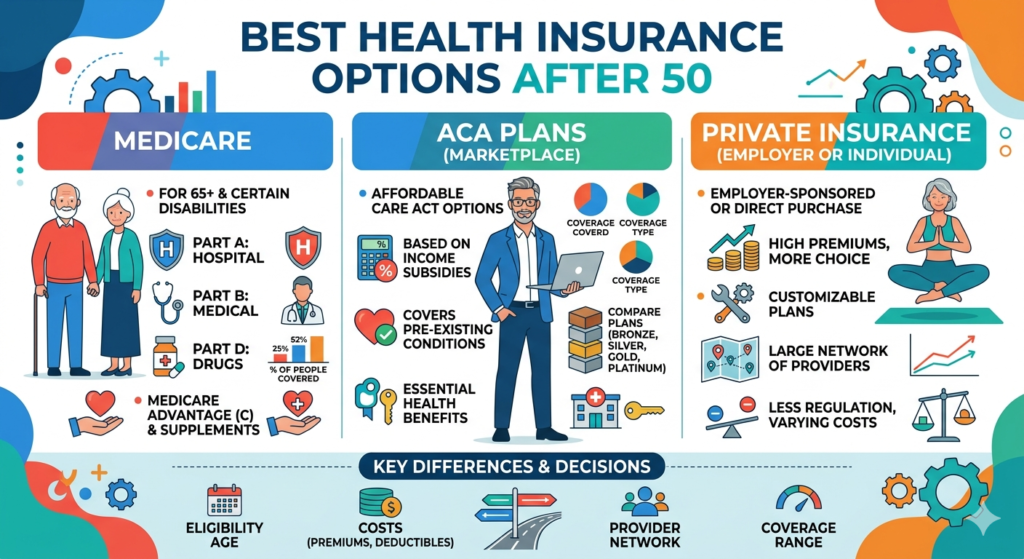

Main Health Insurance Options After Age 50

Let’s explore the most relevant options.

1. Employer-Sponsored Health Insurance

If you’re still working full-time, this is often the best option.

Benefits:

- Lower premiums (shared with employer)

- Comprehensive coverage

- Access to group plans

2. ACA Marketplace Plans (Before Age 65)

If you are not eligible for Medicare yet, ACA plans are a top choice.

Key features:

- Income-based subsidies

- Essential health benefits

- No denial for pre-existing conditions

Plan tiers:

- Bronze

- Silver

- Gold

- Platinum

Best for: Early retirees and self-employed individuals.

3. Medicare (Age 65 and Above)

Medicare becomes available at age 65.

Parts of Medicare:

Part A (Hospital Insurance)

- Covers inpatient care

- Usually free if you paid Medicare taxes

Part B (Medical Insurance)

- Covers doctor visits and outpatient care

- Requires monthly premium

Part C (Medicare Advantage)

- Private plans combining A & B

- Often includes extra benefits

Part D (Prescription Drugs)

- Covers medications

4. Medigap (Supplemental Insurance)

Covers costs not included in Medicare.

Benefits:

- Lower out-of-pocket costs

- Predictable expenses

5. COBRA Coverage

If you leave a job, COBRA allows temporary continuation of employer coverage.

Important:

- Expensive (you pay full premium)

- Temporary (up to 18–36 months)

6. Private Health Insurance

You can buy plans directly from insurers.

Pros:

- Flexible coverage

- Wide networks

Cons:

- Higher cost without subsidies

How Much Does Health Insurance Cost After Age 50?

Costs increase with age.

Average monthly premiums:

- ACA plans: $400 – $900

- Medicare Part B: Standard premium (varies yearly)

- Medicare Advantage: $0 – $100+ (plus Part B)

- Private insurance: $500 – $1,200+

Factors That Affect Cost

- Age

- Location

- Tobacco use

- Income (for subsidies)

- Coverage level

Older individuals generally pay higher premiums.

How to Save Money on Health Insurance After 50

Healthcare doesn’t have to break your budget.

1. Use ACA Subsidies

Lower premiums based on income.

2. Choose High Deductible Plans

Lower monthly cost.

3. Compare Plans Annually

Rates change every year.

4. Use Preventive Care

Many services are free.

5. Consider Medicare Advantage

Often includes extra benefits.

Pre-Existing Conditions: What You Need to Know

After age 50, many people have pre-existing conditions.

Good news:

- ACA plans cannot deny coverage

- Medicare covers pre-existing conditions

This provides strong protection.

Best Health Insurance Providers

Top insurers include:

- Blue Cross Blue Shield

- UnitedHealthcare

- Aetna

- Cigna

- Kaiser Permanente

Each offers plans tailored for older adults.

How to Choose the Right Plan

Step-by-step approach:

1. Evaluate Health Needs

- Do you need regular medications?

- Do you visit specialists often?

2. Compare Total Costs

Look beyond premiums:

- Deductibles

- Copays

- Out-of-pocket maximums

3. Check Provider Networks

Ensure your doctors are covered.

4. Review Prescription Coverage

Important for ongoing medications.

5. Consider Future Needs

Choose plans that support long-term health.

Common Mistakes to Avoid

- Delaying enrollment in Medicare

- Choosing plans based only on premium

- Ignoring prescription coverage

- Not reviewing plans annually

Early Retirement and Health Insurance

If you retire before 65:

Options include:

- ACA marketplace plans

- COBRA (temporary)

- Private insurance

Planning is essential to avoid gaps.

Health Insurance for Couples Over 50

Couples can:

- Choose family-friendly ACA plans

- Enroll separately for better subsidies

- Compare Medicare options individually

Is Health Insurance Mandatory After 50?

There is no federal requirement, but:

- Some states have mandates

- Medical costs can be extremely high

Future Trends in Health Insurance for Older Adults

Emerging trends:

- Telehealth services

- Personalized healthcare plans

- AI-driven diagnostics

- Preventive care focus

Conclusion

Choosing the right health insurance after age 50 is critical for your health and financial security.

Whether you’re using ACA plans, transitioning to Medicare, or exploring private options, the key is to understand your needs and compare plans carefully.

Start planning early, take advantage of subsidies, and review your coverage regularly.

Your health is your wealth — especially after 50.

3. FAQs (Featured Snippet Optimized)

1. What is the best health insurance after age 50?

ACA marketplace plans are best before 65, while Medicare is the top option after 65.

2. Is health insurance pricier after 50?

Yes, premiums generally increase with age due to higher health risks.

3. Can I get health insurance with pre-existing conditions?

Yes, ACA and Medicare plans cover pre-existing conditions.

4. What happens if I retire before 65?

You can use ACA marketplace plans, COBRA or private insurance until Medicare eligibility.

5. When should I enrol in Medicare?

You should enrol at age 65 during your initial enrolment period to avoid penalties.

Disclaimer: The information provided in this article titled ‘health insurance after age 50’ is for educational and informational purposes only. While we strive for accuracy and reliability, we recommend verifying details from official sources or professionals before making decisions.

Also read about the,